Table of contents

Contributions

There are annual super contribution limits, called contribution caps, which guide how much you can contribute to your super that is concessionally taxed. Exceeding these caps, as set each year by the ATO, may result in additional tax liabilities. In this newsletter, we will focus on the two primary contribution types: Concessional Contributions (CC), where we can claim a tax deduction, and Non-Concessional Contributions (NCC), where we cannot claim a tax deduction, which depends on how

much you already have in your Total Super Balance (TSB).

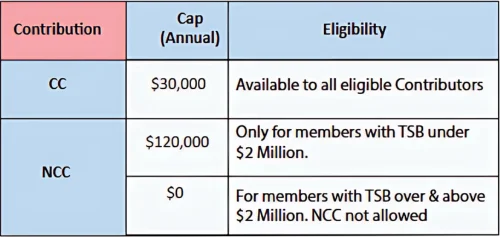

Annual Contribution Caps for F.Y 2025-2026

Concessional contributions (Tax Deductible)

These are contributions for which a taxpayer can claim a tax deduction. However, when received, your super fund pays tax at 15%. These contributions can be made as follows:

Compulsory Employer Superannuation Guarantee (SG) contributions (currently 12% of ordinary time earnings).

Salary sacrifice contributions under an arrangement with your employer.

Personal deductible contributions* (where the individual claims a tax deduction).

Transfers from any reserves to your account which the super fund holds, where applicable.

Important Note: If you're aged 67 to 74, you must satisfy the work test to claim a personal tax deduction. This requires working at least 40 hours within a 30-day period during the financial year.

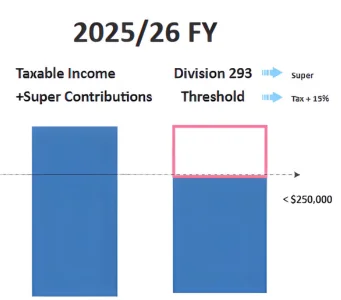

How is Division 293 calculated?

The Division 293 tax equals 15% of the lower of:

The amount by which your income plus concessional contribution exceeds $250,000, or

Your concessional contributions

Example: Division 293 tax calculation

Jan's Division 293 income is $240,000 and her Division 293 super contributions are $15,000, bringing the total to $255,000.

Division 293 taxable contributions are the lesser of:

Division 293 super contributions: $15,000, or

The amount above the $250,000 threshold: $5,000

So, Jan’s Division 293 tax payable is 15% of $5,000 = $750.

Non-Concessional Contributions (After-Tax Contributions)

Non-concessional contributions (NCCs) are voluntary after-tax payments into your super fund. In other words, they come from money on which you have already paid income tax. Because these contributions are post-tax, there is no contributions tax on them (unlike concessional contributions, which are taxed by the super fund).

NCCs effectively allow more of your net income to be added to super to grow your retirement savings.

Carry Forward Rule

If you have contributed less than your concessional contribution cap in any of the last 5 financial years and your Total Super Balance (TSB) is less than $500,000 as at the previous 30 June, then you are eligible to carry forward unused cap space from prior years and contribute more than the annual cap in the current financial year

In effect, your concessional cap in the current year becomes the standard cap plus your accumulated unused amount as calculated below

- Annual concessional cap = $25K (2020–21) and $27.5K (2021–22 to 2023–24) and $30K (2024–25).

- You contributed only $10K each year, so the unused cap accumulated: $15K + $17.5K +$17.5K + $17.5K + $20K = $87.5K.

- In 2025–26, you can use $87.5K carry-forward + $30K current year = $117.5K.

In short: $117,500 can be contributed in 2025–26 provided your TSB is below $500K on 30 June 2025.

Division 293

Tax on concessional contribution can be more than 15% if your taxable income + concessional contribution exceeds $250,000 in 2025- 26 financial year, an additional 15% tax known as Division 293 tax applies.

Concessional contributions are usually taxed at 15%, but if your income plus contributions exceed $250,000,30% tax is applied on all the contributions. For some, it is still beneficial as the top marginal tax rate is 47%, making super contributions still tax-effective.

Common Types of NCCs

- Personal contributions (after-tax): Money you deposit into your super from your own savings.

- Spouse contributions: Payments your spouse makes into your super account.

- Child contributions: Contributions made on behalf of a child under age 18 (from someone other than the child’s employer).

- Foreign fund transfers: Most transfers from overseas superannuation or pension schemes (to your Australian super) are treated as NCCs, provided they aren’t included in your fund’s assessable income

Bring Forward Rule

The bring-forward rule allows you to make up to three years’ worth of non-concessional (after-tax) contributions in one financial year, instead of being limited to the annual cap of $120,000 (from 1 July 2025).

How much you can contribute depends on your total super balance as at 30 June of the previous year.

- If your balance is less than $1.76M, you can contribute up to $360,000 over 3 years using the bring-forward rule.

- If your balance is $1.76M to less than $1.88M, your cap is $240,000 over 2 years.

- If your balance is $1.88M to less than $2M, you can only contribute $120,000 for the year; no bring-forward applies.

- If your balance is $2M or more, you cannot make any non-concessional contributions.

Other Types of Contributions

There are other types of contributions such as:

- Downsizer Contributions

- First Home Super Saver Contributions

- Government Co-Contributions

- Contributions due to Sale of Small Business

If you need any further information or guidance on Super Contributions, please contact our office