Table of contents

Digital assets in Super

In this newsletter, we'll explore how your SMSF can invest in cryptocurrency and what you need to watch out for. With digital assets like Bitcoin and Ethereum gaining popularity, more trustees are considering crypto as part of their fund's long-term investment strategy.

Cryptocurrency may be a modern asset, but your SMSF still plays by traditional rules. The ATO expects full compliance with the Superannuation Industry (Supervision) Act (SISA), Regulations (SISR), and the SMSF's own trust deed.

Over the past five years, the value of crypto assets held by SMSFs have grown dramatically—from just $198 million in March 2020 to $1.68 billion by March 2025. This sharp rise reflects a growing appetite among investors for alternative investments and signals a shift in how retirement portfolios are being diversified.

What's drawing SMSFs into the world of crypto?

Cryptocurrency is a type of digital asset—often called a "digital coin"—that can be used to buy, sell, or exchange online. Despite its ups and downs, crypto attracts SMSF investors looking for high-growth opportunities beyond traditional assets.

Can your SMSF really invest in crypto?

Yes, SMSFs can invest in cryptocurrency—but only within a strict compliance framework. For the investment to be valid, it must be permitted under the fund's trust deed and clearly outlined in the SMSF's investment strategy. Without proper structure, documentation, and a clear link to the fund's retirement goals, even a single crypto transaction could lead to serious compliance issues.

The First Compliance Gate: SMSF Trust Deed

Before diving into cryptocurrency, the first step is to review your SMSF trust deed. This legal document must explicitly allow investment in cryptocurrency or digital assets.

It should also provide trustees with the discretion to invest in a wide range of asset classes, including non-traditional or alternative assets like crypto. Most importantly, it must align with the SMSF's core obligation: to provide retirement benefits to its members.

If your trust deed is outdated or doesn't mention digital assets as an allowable asset class, investing in crypto may be a breach of superannuation law—even if the intention is good.

Many older deeds were created before cryptocurrency existed and lack the necessary flexibility. But having the right deed is just the starting point. Once that's in place, your SMSF must also comply with several key legal and regulatory requirements under the SIS Act and Regulations:

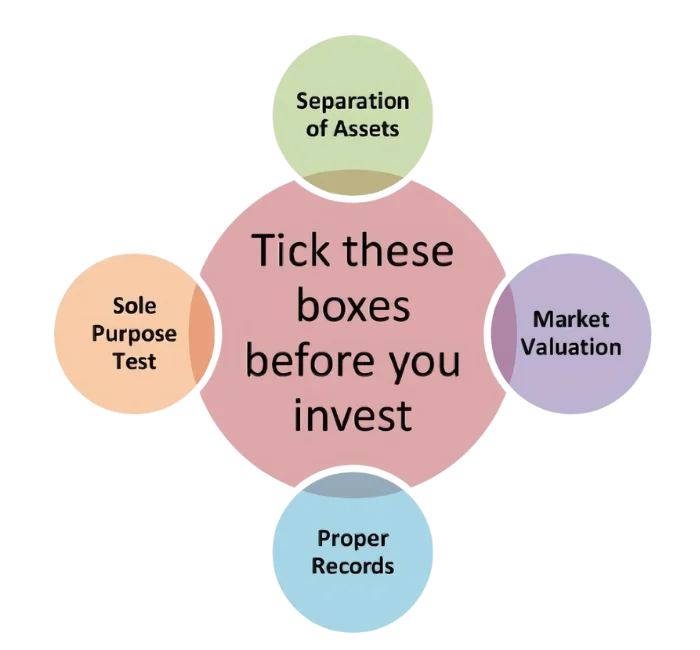

Sole Purpose Test - SISA Section 62

Any crypto investment must be made solely for the purpose of providing retirement benefits to members (or their beneficiaries).

Using SMSF crypto assets for day trading, speculation, personal use, or short-term gain puts your fund at risk of breaching this fundamental rule.

Separation of Assets - SISA Section 52B(2)(d)

All SMSF assets must be kept completely separate from members1 personal assets—including crypto.

The crypto currency must be held in a wallet or exchange account in the name of the SMSF, with no overlap in control, access, or email addresses between fund and personal holdings. No exceptions.

Market Valuation - SISR Regulation 8.02B

Crypto must be recorded at fair market value at the end of each financial year. The valuation must be based on objective, supportable data—such as price feeds from reputable exchanges—and clearly documented for audit purposes.

Proper Records - SISA Section 35A

You must maintain clear and accurate records of all crypto transactions: acquisitions, disposals, transfers, valuations, and wallet addresses. These records should demonstrate the fund's ongoing compliance and be readily available for review.

Crypto in SMSFs: Cool Asset, Hot Risk

If you don't get the setup right, the ATO won't care how smart your investment was. Cryptocurrency is no longer a fringe idea. SMSFs are dipping into Bitcoin, Ethereum, and beyond.

But here's the truth: the ATO isn't watching crypto—they'rewatching you - So, before your SMSF invests in Bitcoin or Ethereum, get these non-negotiable rules right:

- The Wallet Must Be in the Fund's Name

Personal wallet = personal asset. If the wallet isn't legally owned by the SMSF, the investment may not count—and you could breach the SIS Act. - Keep Personal and SMSF Crypto Worlds Apart

One wallet for you. One for the fund. Mixing assets is a compliance nightmare and one of the fastest ways to fall foul of superannuation law. - Stick to Reputable Exchanges

Don't get burned by dodgy platforms. Use licensed, secure, and transparent exchanges. If it looks shady, it probably is— and the ATO won't be sympathetic. - Record Everything—Yes, Everything

Every transaction matters. From swaps to sales, keep detailed records for tax, audits, and capital gains calculations. If it's not documented, it didn't happen. - Guard Your Wallet Like It's Your Super (Because it is)

Lose your password, lose your crypto. Keep access details secure and offline. And make sure that you are not the only trustee who has the password - because should anything happen to you - the asset will be lost forever. - No Favoritism—Even with Related Parties

Deals must be at arm's length. That means market value, proper contracts, and no "mates' rates." Anything less can trigger Non Arms Length penalties. - Valuation Isn't Optional

You'll need year-end valuations backed by real market data. Guesswork won't cut it—your auditor will need proof.

Tax Treatment of Crypto Assets

Crypto assets can be bought, sold, or exchanged—whether through a trading platform or directly via a digital wallet. They can also be used to pay for goods and services.

The way you use crypto determines how it's taxed:

- For most investors, including SMSFs, crypto is treated as a capital gains tax (CGT) asset. Profits made from selling, swapping, or disposing of crypto are subject to CGT.

- Staking rewards and similar blockchain-based earnings are considered ordinary income and must be reported accordingly.

Getting the tax treatment right is crucial for compliance— especially in an SMSF context, where record-keeping and audit requirements are stricter.

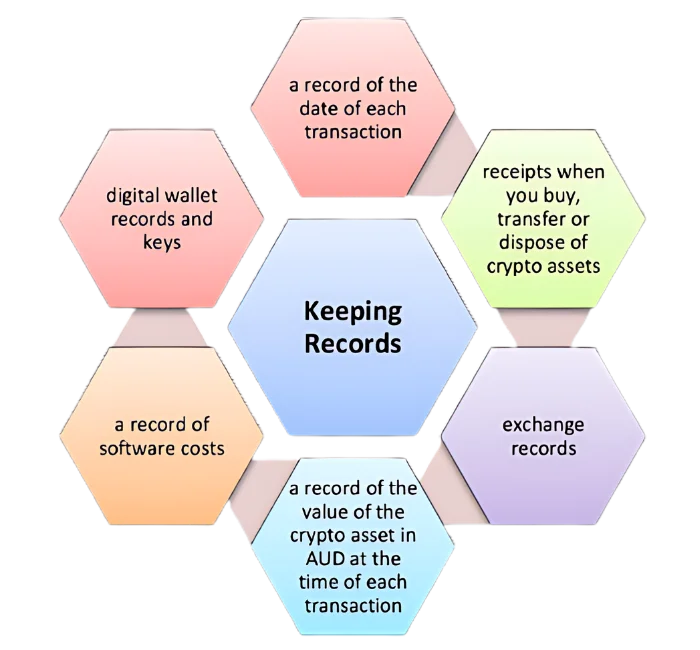

Keeping Crypto Records

Crypto currency in SMSF

The ATO is looking at crypto as an asset class, it is placing increasing scrutiny on how trustees handle ownership, documentation, and compliance obligations.

As a trustee of your SMSF, you are responsible for ensuring that all crypto investments are structured and managed correctly. Common issues—such as using personal wallets, failing to demonstrate legal ownership, or blurring the lines between fund and personal assets—can put the SMSF at serious risk.

With digital assets now firmly on the ATO's radar, clear documentation, strict asset separation, and compliance with the trust deed and investment strategy are not just best practice—they're essential safeguards.

Before you invest, transfer, or stake crypto within your SMSF, please contact our office. We can assist you with:

Setting up of SMSF trust deed or updating the deed which allows investing in crypto currency and there's a right way to invest in Crypto in SMSF —and we're here to help you get it right.